The consumer financial technology industry has faced its fair share of challenges this year. From turmoil in the banking sector (we’re looking at you, Silicon Valley Bank and First Republic) to rising interest rates, it hasn’t been smooth sailing.

Yet, despite these adversities, millions of consumers have access to considerable financial betterment thanks to the progress of consumer financial technology.

In a global context, the fintech boom is running parallel to remarkable growth in financial inclusivity. Per the Global Findex Database, 76% of the world’s adult population had a bank or mobile account in 2021, marking a substantial rise from the 51% recorded in 2011.

So what’s next for the consumer financial technology sector in 2023?

Here are our top trends and predictions.

What is consumer financial technology?

Consumer financial technology, commonly known as fintech, represents the dynamic intertwining of financial services and modern technology aimed at the everyday consumer.

In other words, using technology to drive a profound evolution in how we manage, spend, save, and invest our money.

At its core, consumer financial technology exists to streamline and simplify financial operations that were traditionally cumbersome or inaccessible to the average person.

Here are a few examples:

- Mobile banking

- Peer-to-peer transfers

- Digital wallets

- Robo-advising

- Personal financial management

- Lending

As revealed by Plaid’s 2021 impact survey, fintech found a warm embrace in the digital pockets of US consumers. An impressive 90% of Americans leveraged fintech in 2021, marking a 52% annual spike in adoption.

And more interestingly, the survey highlights that 80–90% of these fintech aficionados intend to maintain, if not increase, their reliance on these tech-driven financial tools moving forward.

So, whether paying for your morning coffee with your smartwatch or managing your investment portfolio from an app, you’re engaging with consumer financial technology.

So, how does this flourishing fintech adoption translate into the future? Here are our five emerging trends and predictions on the fintech horizon.

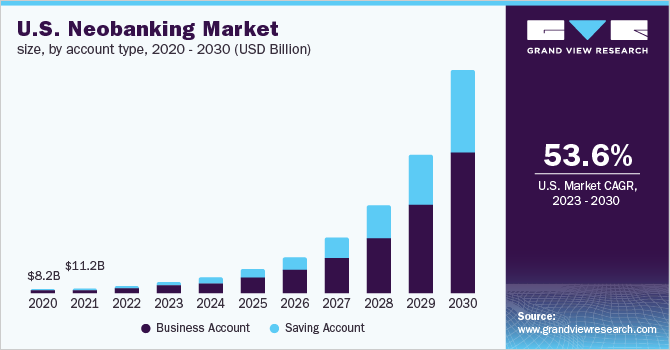

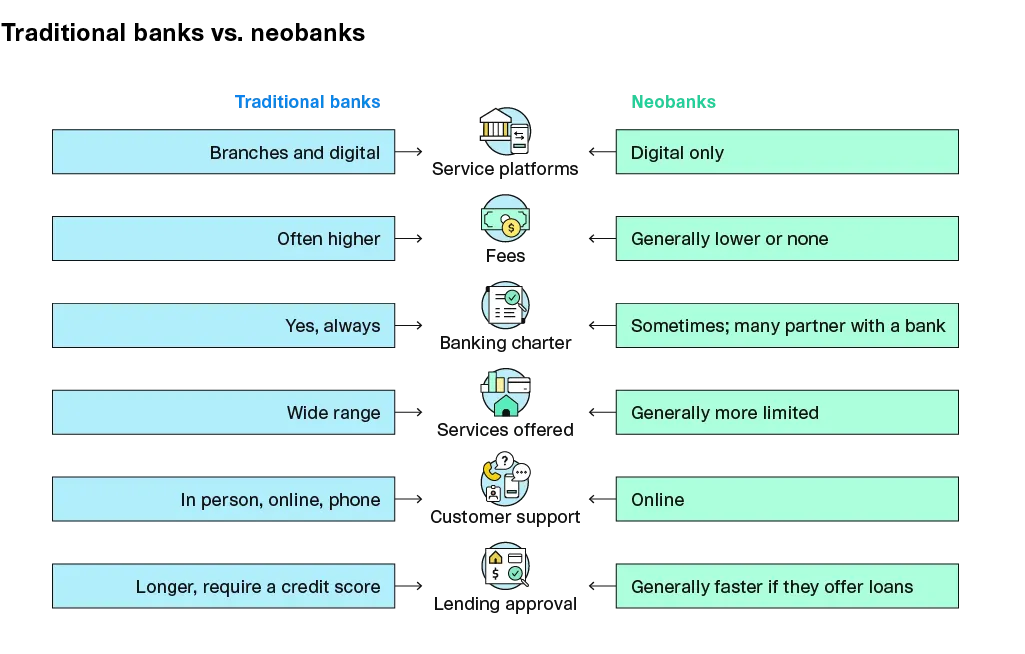

1. Neobanks will pull away with a clear competitive advantage

Neobanks, the digital-first, branchless cousins of traditional banking entities, are set to gain considerable traction on the fintech freeway growing at a compound annual growth rate (CAGR) of 53.6%.

Essentially, neobanks exist entirely online, providing a comprehensive suite of banking services sans the physical infrastructure of conventional banks.

The intrinsic charm of neobanks lies in their ability to offer more competitive products. Free from the substantial overhead costs associated with brick-and-mortar operations — think buildings and maintenance — neobanks have the luxury of passing on these savings to their consumers.

The cost advantage can appear in the form of higher interest rates on savings accounts, lower loan rates, or minimal to zero fees on transactions and account maintenance.

For example, Chime, the largest neobank by user base, offers a variety of benefits, including:

- Pay friends and family fee-free regardless of what bank they use

- Get paid two days early with a direct deposit

- No overdraft fees

- No minimum balance

- No monthly fees

- No foreign transaction fees

- Access to 60,000+ fee-free ATMs

So not only does this edge make neobanks a top fintech contender, but it also redefines consumer banking expectations. Digital, convenient, and cost-effective financial services are the new norm.

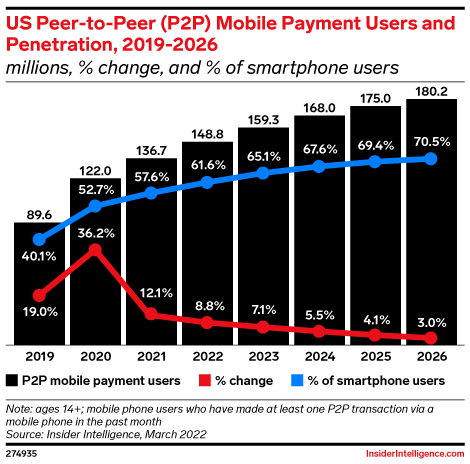

2. Consumers shift toward real-time payment solutions

When it comes to our money, we have zero patience. We want our money, and we want it now.

Thanks to technological advancements, this consumer demand is now attainable. Enter: peer-to-peer (P2P) payment solutions. Nearly 160 million Americans will make P2P payments in 2023, thanks to the allure of simplicity and speed.

P2P payment solutions offer an instant, convenient, and usually cost-effective way to transfer money directly between individuals — all via the click of a button on a smartphone or computer.

Whether splitting a dinner bill or sending a birthday gift to a loved one, P2P payments reduce the need for cash, credit cards, and checks. The result? Swift, seamless, and secure transactions.

The consumer shift towards P2P solutions is a testament to the increasing demand for financial services that marry convenience with control. Integrating these payments with an online budget app can further streamline personal finance management, allowing consumers to track and manage their spending and transfers all in one place. Even the Federal Reserve is jumping on the bandwagon with the launch of the FedNow Service in July.

The FedNow Service service acts as a bridge for interbank clearing and settlement. The set-up opens the door to facilitate an instantaneous flow of funds from the sender’s account to the receiver’s — regardless of the time or the day (read: holiday or weekend).

The beauty of this solution is to finally abolish inconvenient banking hours by offering 24/7/365 availability.

Here’s where it makes a world of difference: picture yourself selling your business. Traditionally, such a material transaction could entail an excruciating waiting period for the incoming payment to arrive in your bank account, opening the door to unnecessary stress and uncertainty.

With the FedNow Service, such concerns will be a thing of the past. Payments can be expedited in near real-time, slashing the time you spend in this payment limbo and significantly reducing the anxiety associated with such significant transactions.

But it doesn’t just apply to selling a business. It could be any transaction that involves a high-ticket item, such as selling your car or making a downpayment on your first house. It’s convenient and keeps your mind at ease. What’s not to love?

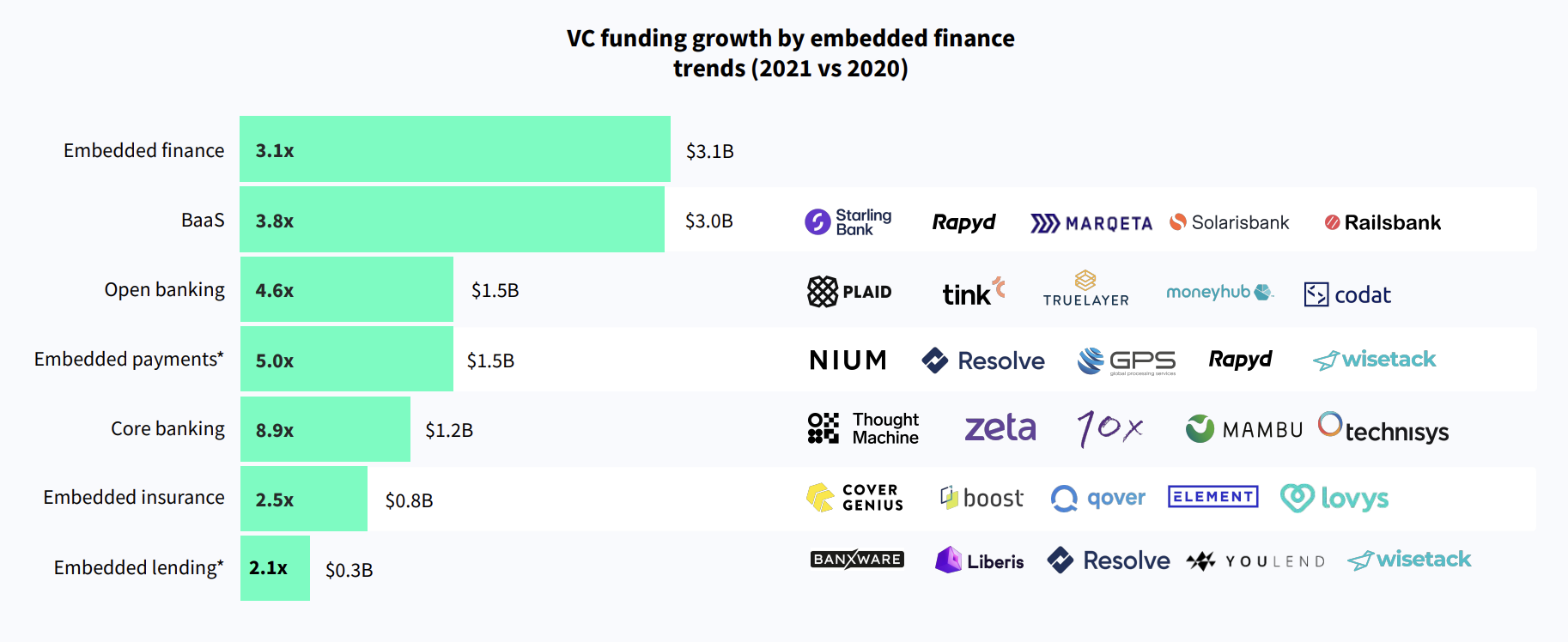

3. Embedded finance is the topic of the year

Embedded finance isn’t a novel concept — think of United Airlines’ private-label credit cards or auto loans at car dealerships. These arrangements have traditionally acted as ways for banks to engage with customers while providing a “value add” front for the partner.

However, what sets the next wave of embedded finance apart is the fusion of financial offerings with digital touchpoints that users frequent daily. Consider customer loyalty apps like Starbucks or digital wallets like Apple Wallet.

Businesses are evolving to meet customers’ financial needs by adding banking services to existing product ecosystems.

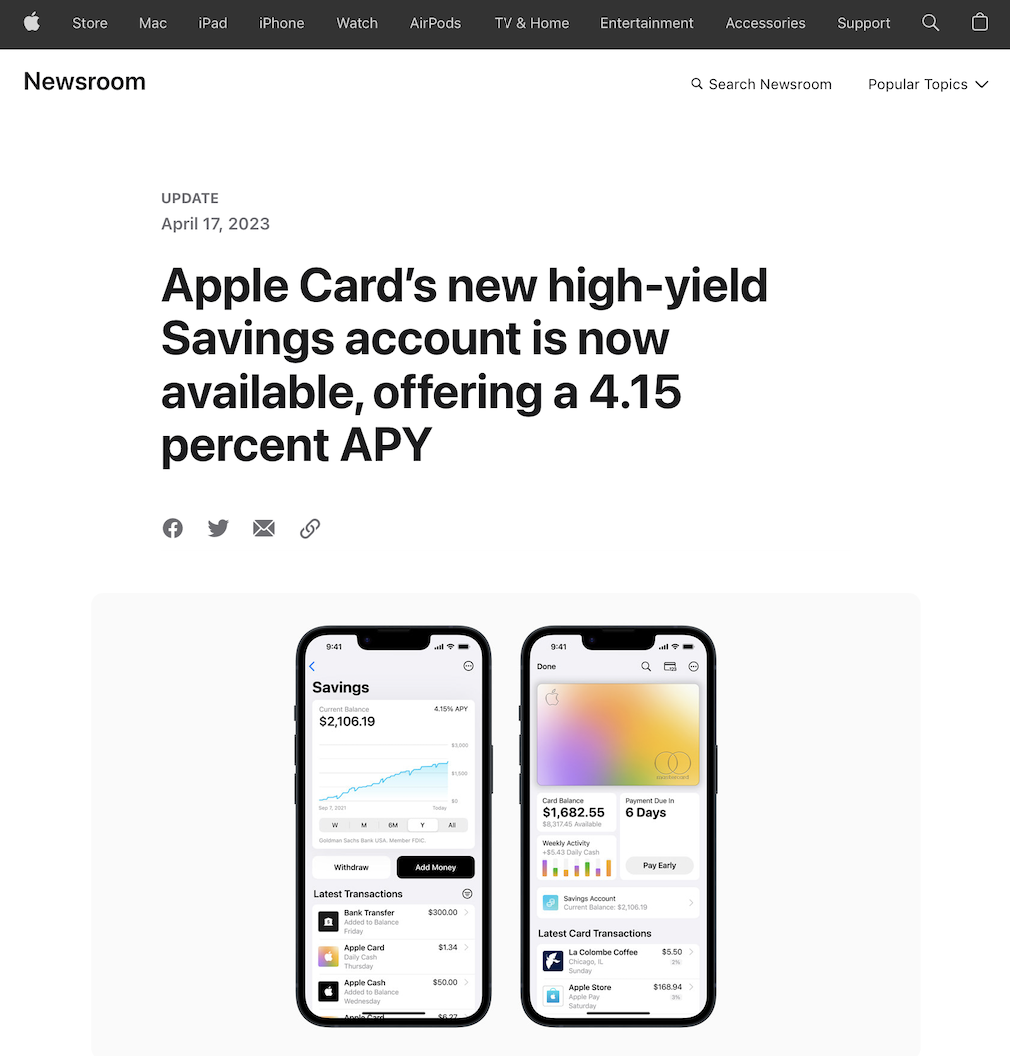

In fact, according to Ralph Dangelmaier, CEO & Board Member at BlueSnap, the April 2023 announcement of Apple’s 4.15% high-yield savings account is a prime example of embedded finance in action.

He states, “…the savings account is a sure sign that Embedded Banking is taking hold. Apple Card owners and co-owners can easily and seamlessly open a Goldman Sachs savings account from within their Apple wallet, and Apple Cash is instantly deposited into that savings account.

This is a far cry from walking into a bank branch or opening an account online on a bank website and then manually typing in the account number and routing number into an app. It’s all about convenience, ease, and trust.”

This seamless blend of finance and digital interactions fuels the powerful promise of embedded finance.

But this disruptive trend isn’t just rewriting the rulebook of financial services. It’s also attracting a flood of investments from venture capitalists. All-in-one investing is trending as people generate cash through safe and intelligent investments.

The powerful combination of tech-enabled financial services and customer-centric business models is proving to be an irresistible opportunity for investors.

Embedded finance is one of the hottest tickets in the consumer financial technology industry, with the potential to create synergistic partnerships and unlock a treasure trove of value.

4. Personalization takes center stage to appeal to younger generations

Today’s younger generations, notably Gen Z, are increasingly shifting their trust from traditional banking institutions to fintech companies.

This trend is not accidental but conscious business decisions by these companies to provide personalized services that meet the specific needs and expectations of these tech-savvy demographics.

After all, a 2021 EY study reveals that 81% of Gen Z agree that personalization would strengthen the relationship with a financial services company.

But what should that personalization look like?

- Guidance on how to fully leverage the benefits of their current products

- A deep understanding of their interests and priorities

- Timely product suggestions tailored to their needs

- Customizable product features

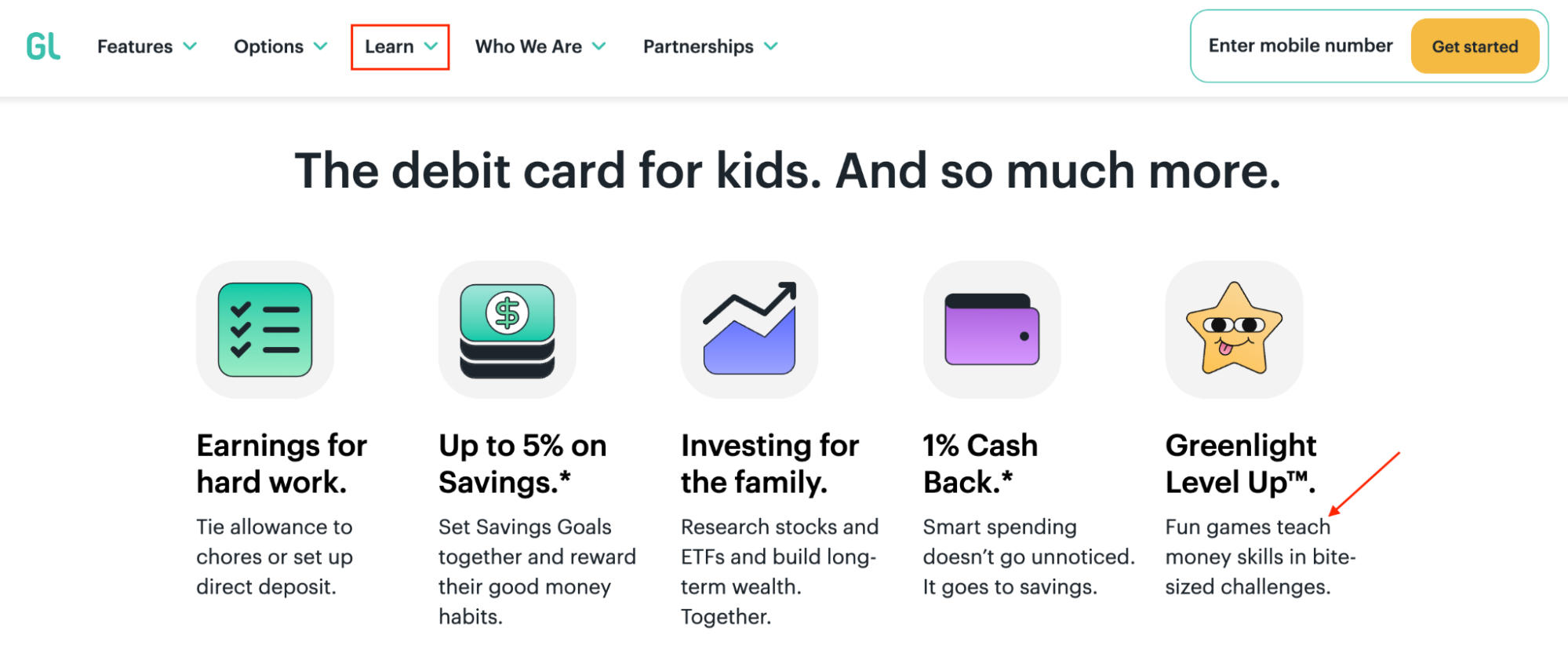

One example of this trend is the rise of teen debit cards. These aren’t simply smaller versions of their adult counterparts. These debit cards include access to tools and apps that educate the younger generation about financial responsibility.

It also provides them with some degree of financial independence and personalization.

Consumers don’t want to feel like a number on a spreadsheet. They want to leave every interaction feeling understood and valued as a customer.

Fintech firms that ditch the one-size-fits-all approach to traditional banking and instead focus on a flexible, user-focused model — like a hybrid office using a desk booking system — will come out on top.

5. Data security remains a top consumer priority

Just because consumers enjoy the convenience of digital experiences doesn’t mean they’re willing to compromise security.

The numbers speak for themselves. According to recent studies, an overwhelming 90% of consumers express concern about banking or credit fraud as financial services increasingly pivot towards a digital approach.

The message is clear: data security is no longer just an option. It’s a non-negotiable.

Enter open authorization, artificial intelligence, and machine learning — technologies at the forefront of tackling these security concerns head-on.

Open Authorization, or OAuth, acts as a digital gatekeeper. It provides a secure, efficient way for users to grant applications access to their data without sharing sensitive credentials. It’s likely to become a standard protocol in fintech, providing secure and convenient access and boosting consumer confidence.

Meanwhile, artificial intelligence (AI) and machine learning (ML) are powerful tools that provide proactive, intelligent solutions to mitigate risks. AI and ML capabilities range from real-time fraud detection to spotting potential cyber security threats, adding an advanced level of protection.

But, it’s not enough to just implement these technologies. Brands must regularly communicate their security protocols, underlining their commitment to data safety.

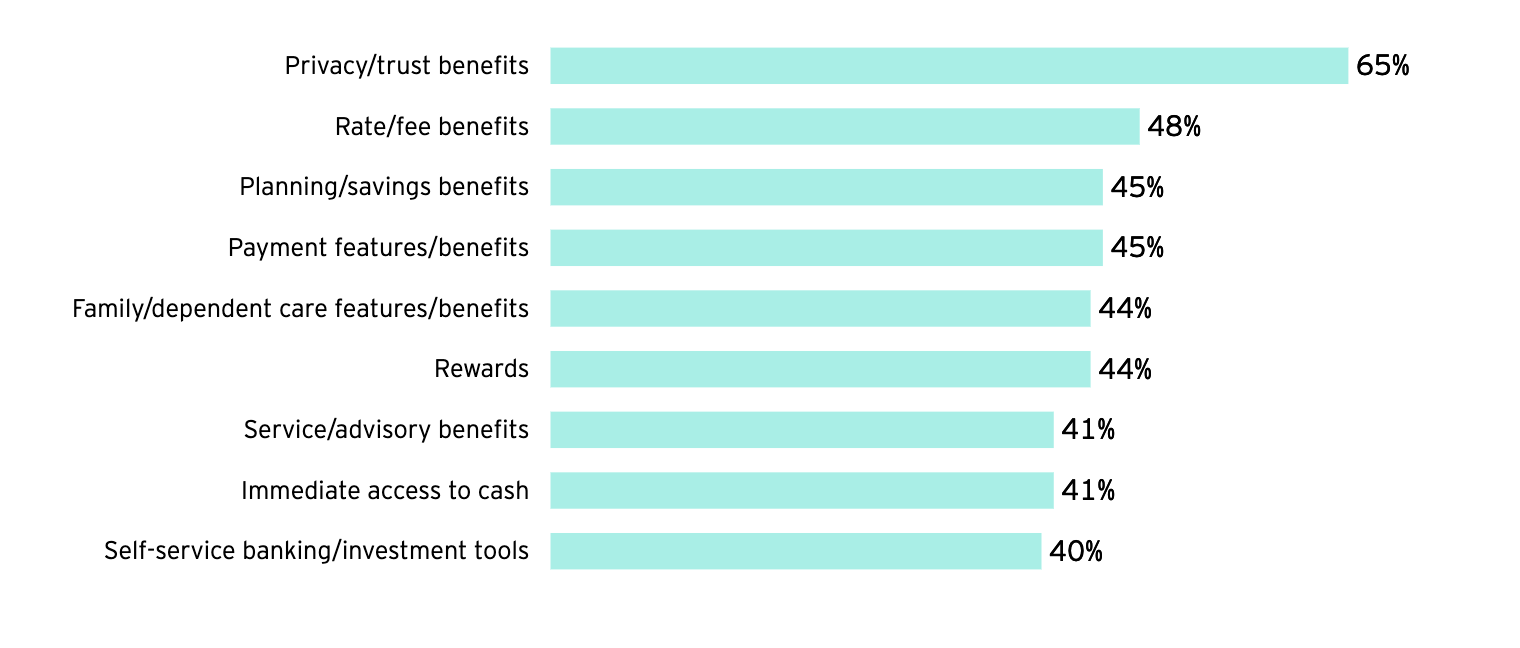

Such transparency is crucial in fostering trust, a quality considered a top priority by 65% of consumers when choosing a fintech brand.

The future of consumer financial technology and data security go hand and hand. And brands prioritizing data security will rise above the competition, providing a platform that consumers genuinely trust.

Wrapping up

Every leading fintech trend revolves around one key player: the consumer. Fintech’s growth is rooted in its focus on serving consumers in innovative ways. And these trends reflect changing consumer demands and fintech’s ability to adapt swiftly.

Consumer financial technology’s future is bright, filled with opportunities for those ready to seize them. But the capacity to innovate and adapt will determine the organizations that’ll pull ahead in this fast-paced and competitive sector.

And those that make finance more inclusive for all will win over the hearts of consumers.